A donor advised fund (DAF) is a philanthropic giving vehicle with the flexibility to invest in a variety of asset types.

Downloads

Key Elements

- Charitable investment vehicle with immediate tax benefits for donors

- Flexibility to disperse different capital products like grants, equity, debt, or fund commitments

What is a DAF?

DAFs started in the US during the 1930s as philanthropic giving vehicles that enabled donors– individuals, families, companies, or institutions– to invest in a variety of asset types while receiving immediate tax benefits.

Following a DAF contribution, a donor maintains control over the timing of grant distributions to charitable organizations from that DAF, but they also receive tax benefits for charitable contributions based on the timing of contributions to the DAF.

DAFs are created and administered by a sponsor such as community foundations (e.g. Silicon Valley Community Foundation), national charities (e.g. ImpactAssets and Fidelity Charitable), and single-issue charities (e.g. universities and faith-based charities). As of 2021, DAF sponsors held $160B+ in assets under management (AUM).

Here are four proven mechanisms for investors leveraging DAFs to support underrepresented entrepreneurs and fund managers:

- Make a grant from DAF to a nonprofit intermediary that supports underrepresented entrepreneurs or fund managers.

- Make a debt investment from DAF to a nonprofit intermediary that supports underrepresented entrepreneurs or fund managers.

- Make a grant from DAF to a for-profit organization that qualifies as charitable.

- Make an equity or debt investment from DAF to a for-profit organization or for-profit intermediary. (e.g. Capital Access Lab, MIT Solve Innovation Future, and PRIME Coalition).

Case Studies

View All

Capital Access Lab Case Study

MIT Solve Innovation Future Case Study

FAQs

Yes, a DAF can make both direct and fund investments.

Donors and DAF sponsors might have to pay excise taxes if the DAF investments or distributions do not align with the donors’ charitable purpose.

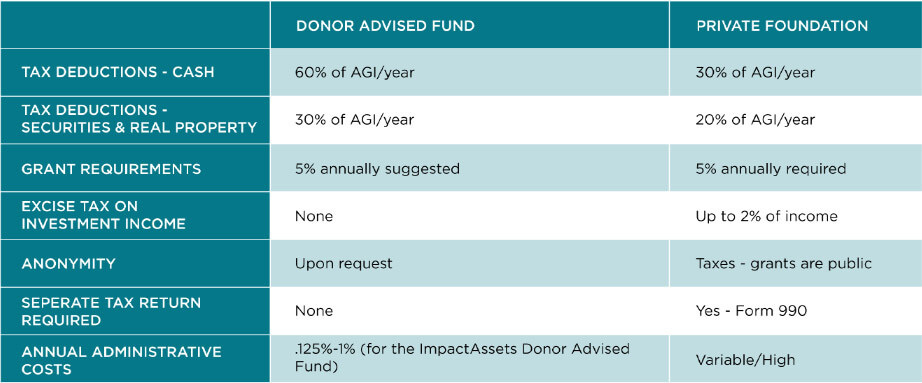

Tax benefits for donors include avoiding capital gains taxes and receiving a federal income tax deduction of up to 50% of adjusted gross income (AGI) for cash contributions. More tax advantages are listed below.

Source: ImpactAssets

Yes, donors can contribute non-cash assets like real estate, stock, and crypto to DAFs and receive immediate tax benefits.

Deeper Dive

When is a DAF a good fit for capital providers?

- Cheaper & Faster Launch: Compared to a traditional GP/LP fund structure, a DAF is easier and faster to set up and launch for investors.

- Tax Efficiency: Taxable investors, including individuals and families, can receive immediate tax benefits and postpone charitable giving by contributing to a DAF.

- Access to Philanthropic Capital: Many donors leverage DAFs as a way to offset their high income years with flexible charitable giving. DAFs allow donors to have more time to decide when and how they will make distribution to charities. Investors can either launch their own DAF vehicles to attract philanthropic capital or market their funds to DAF platforms.

- Flexible Investment Options: DAFs have the flexibility to invest in a wide variety of assets, including startups, small businesses, real assets, and fund managers. Additionally, DAF managers have the flexibility to make equity, debt, and innovative investments or grants.

When is a DAF not a fit for capital providers?

- Raising Capital beyond Donors: The DAF vehicle allows investors to raise philanthropic capital, but it does not allow investors to raise other types of “LP” capital. Investors need to set up investment vehicles beyond DAFs, such as 506(b) or 506(c) funds, to accept other sources of LP capital.

- Investments outside of Charitable Purpose: DAF managers need to align their impact investments with the donors’ charitable purpose. Otherwise, the DAF managers and sponsors are subject to excise taxes for investments outside of their charitable purpose.

What should capital providers look out for with DAFs?

- Philanthropic Signal: DAFs can be a powerful financing tool for early-stage entrepreneurs and fund managers; however, potential coinvestors and follow-on investors may view DAF capital as a signal for concessionary returns.

- Potential Tax Shelter: DAFs can be used as a tax shelter for donors as their contributions sit in DAFs for years before they decide to grant them to charities. Donors do not need to invest their DAF contributions in mission-driven organizations or assets. A small percentage of the $110B+ in DAF capital across the US was invested for impact.

Costs

What do DAF sponsors typically charge for DAFs?

- Administrative Fee: tiered fee levels based on AUM.

- First $100K: 1.00% annual fee

- Next $400K: 0.75%

- Next $500K: 0.50%

- Next $9M: 0.25%

- $10M+: 0.125%

- Investment Administrative Fee: additional fees per investment the DAF makes.

- First $100K: 0.80%

- Next $100K: 0.60%

- $200k+: 0.40%